Hope is Never a Great Investment Strategy

There is a great deal of discussion in the financial media by professional investors expressing a hope for the so-called “soft landing” as the Fed continues to fight inflationary pressures. Much of what was written and said in the week just passed reflected such hope-filled sentiment in reaction to a rally in stocks so far this year. There is no question, the rally is impressive.

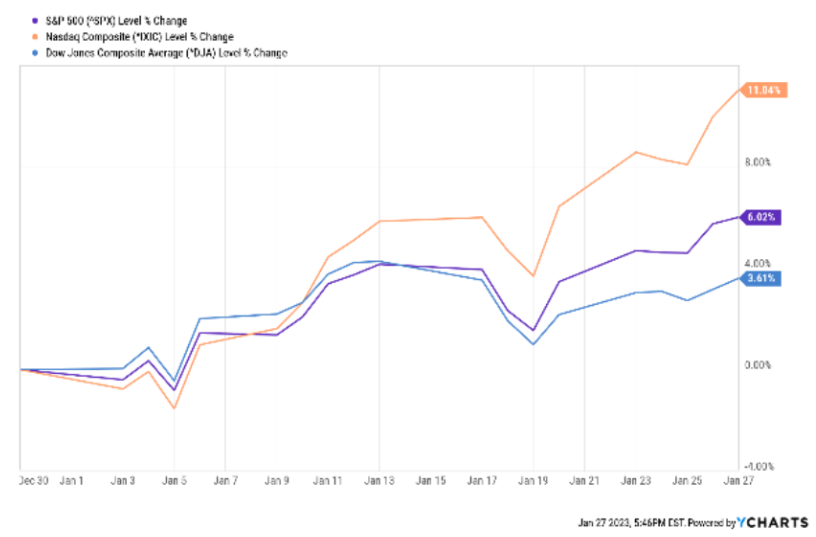

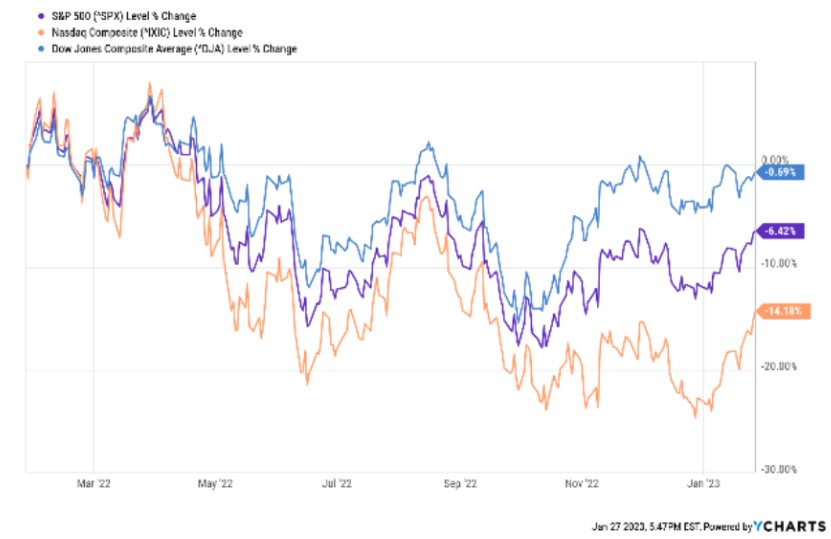

Here are two charts for the stock markets: 1) The year-to-date chart on the left, and 2) the one-year chart on the right.

The year-to-date chart on the left above shows a big move, especially in the NASDAQ index which is up over 11%, while the S&P is up 6% and the Dow almost 4%. When comparing the year-to-date chart to the one-year chart, we can see that the Dow is the leader down for one-year less than 1%. The S&P is down over 6% while the NASDAQ is down over 14%. What are we to conclude from the information available to us combined with the charts above?

- Stocks have come down in price primarily because interest rates have gone up as the Fed fights inflation. Given that stocks are valued by discounting their future earnings by prevailing interest rates, a downward move makes sense.

- It also makes sense that the technology dominated Nasdaq is down most over the year because tech stocks and growth stocks were the most over-valued at the start of the correction.

- Does the rally in January so far make sense? We think the answer is that the rally in January makes sense ONLY if the Fed is done raising rates AND there is no material decline in corporate earnings.

- Both a call for a soft landing and a Fed pivot have been referenced frequently in the financial press as the primary reasons for the rally. But are these expectations realistic? Maybe, but probably not.

- We think it is far too early to make that call. We are in the midst of corporate earnings season and so far, it appears fourth quarter earnings will experience year-over-year declines of about 5%. Moreover, as of this writing, according to FactSet, bottom-up analyst expectations are calling for year-over-year earnings declines in the first and second quarters of 2023.

- So, it feels too early, particularly with the Fed still fighting inflation by raising rates and the specter of an economic recession still threatening.

- Given all this, we think it is better to expect continuing bouts of market volatility and continuing stock price pressures as we walk through the unfolding economic realities in the coming weeks and months.

There is ‘hope” the market correction is over. There is “hope” the Fed will soon pivot. Finally, there is “hope” a recession will be avoided, and a soft landing will be orchestrated. We may find that the hope-fueled rally is a respite in a longer-term period of market consolidation. Or it might be the real deal. But remember, hope is never a good investment strategy. In the meantime, enjoy the rally while it lasts and make sure your portfolio appropriately reflects your risk tolerance.

Advisory services offered through WealthPlan Group, a DBA for WealthPlan Investment Management, a subsidiary Registered Investment Advisor of WealthPlan Group, LLC. WealthPlan Group, LLC is not a registered investment advisor, but is the holding company for WealthPlan Partners LLC and WealthPlan Investment Management, LLC.

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which Investment(s) may be appropriate for you, consult your financial advisor prior to investing. Information is based on sources believed to be reliable, however, their accuracy or completeness cannot be guaranteed.

No investment strategy can assure success or completely protect against loss, given the volatility of all securities markets. Statements of forecast and trends are for informational purposes and are not guaranteed to occur in the future. All performance referenced is historical and is no guarantee of future results. Securities investing involves risk, including loss of principal. An investor cannot invest directly in an index.

The information in this communication applies solely to the intended audience and in no way amends, revokes, or otherwise alters the existing agreements and relationships between WPIM and its clients. This communication is not a binding offer, expressed or implied. WPIM undertakes no obligation to update or revise the information herein or in any referenced third-party resource due to new information, future events or circumstances, or otherwise.

WealthPlan Investment Management (“WPIM”) uses data compiled and/or prepared by third parties (“Third Party Data”) in the delivery of Licensed Research and Data. Third Party Data is not owned by WPIM and user may be required to obtain permission directly from third parties for further use of Third-Party Data and may be required to pay a fee depending on the use contemplated by the user.